Wall Street Sees 53% Upside in Workday Stock. Is WDAY a Buy Now?

/AI%20(artificial%20intelligence)/Artificial%20Intelligence%20AI%20by%2013_Phunkod%20via%20Shutterstock.jpg)

Workday (WDAY) just delivered another quarter that showed why it has become a one-stop platform for businesses looking to integrate human resources and finance in the age of artificial intelligence (AI). With both top-line strength and operational discipline, Workday demonstrated that its customer adoption, AI-driven innovation, and platform expansion strategy are paying off.

Workday stock has dipped 12.9% year-to-date, compared to the broader market gain. Nonetheless, Wall Street forecasts potential upside of 53%.

Workday Is Positioned for Durable Growth

Workday is a cloud-based software company that helps businesses manage their employees and finances. Its platform is used for payroll, hiring, and performance reviews, as well as budgeting, expense management, and accounting. Workday reduces enterprise complexity and cost of ownership by managing people and money on a single AI-native platform, while also providing speed and precision in decision-making.

In the second quarter of fiscal 2026, customer adoption increased across healthcare, government, financial services, technology, and education, demonstrating the Workday platform’s broad relevance. Subscription revenue increased 14% year over year (YoY) to $2.17 billion. Total revenue increased by 12.6% YoY to $2.4 billion. Adjusted earnings increased 26.3% to $2.21 per share.

Total subscription revenue backlog stood at $25.37 billion, with current RPO at $7.91 billion. At the end of the quarter, cash and marketable securities totaled $8.2 billion. The company also repurchased $299 million in stock, reflecting confidence in its long-term value creation.

In the quarter, Workday made it clear that India is a key component of its future strategy for long-term, sustainable growth. The company announced plans to launch services in the country through a local data center. It also began expanding its teams and partner ecosystem in the region. Workday is laying the groundwork in a market where AI, digital transformation, and workforce modernization are accelerating.

Furthermore, Workday continues to position AI as a tool to help people achieve their full potential, rather than a replacement. With Workday Illuminate, which it claims is the largest and cleanest finance and HR dataset in the industry, the company is positioning itself to deliver highly relevant AI-driven insights and automation across enterprises. Workday has a significant moat, with over 75 million users under contract and a trillion transactions processed last year alone.

In the second half of the year, the company intends to prioritize scaling AI innovation, driving full-suite adoption, and expanding global reach. Following a strong first-half performance, Workday increased its full-year fiscal 2026 guidance. Subscription revenue could increase by 14%, reaching $8.8 billion. CEO Carl Eschenbach stated, “We’re building for the long term while executing in the near term — and I couldn’t be more excited about what’s ahead. When we put AI to work for people — not in place of them — we unlock potential we’ve only begun to imagine.”

Workday’s emphasis on India, AI-powered innovation, and unified finance and HR platform positions it well to capitalize on a growing total addressable market. Investors should watch out for Workday’s upcoming Workday Rising conference and Financial Analyst Day on Sept. 16. The company intends to disclose more information about its AI roadmap, new product innovations, and long-term growth and margin expansion strategy.

What Are Analysts Saying About Workday Stock?

Following the Q2 earnings, Citi analystSteven Enders held on to his “Neutral” rating and lowered WDAY’s target price to $260 from $279. Enders found the second-quarter results to be mixed, and he is cautious about the company’s upcoming analyst day and near-term outlook.

Similarly, Canaccord lowered its price target to $275 from $330, while maintaining a “Buy” rating on the stock. According to the firm, Workday’s second-quarter results exceeded the high end of its revenue and earnings guidance. However, management was cautious when discussing the potential impact of its recent acquisition of Paradox, a recruitment automation platform, claiming that it was too early to quantify the inorganic contribution. Furthermore, the firm noted that, while Workday’s backlog growth improved significantly in Q2, the company clarified that much of this strength was due to customer-led early renewal activity rather than new deal acceleration. These conflicting signals prompted the firm to lower the target price.

On the other hand, Bank of America Securities analyst Bradley Sills maintained a positive outlook, reaffirming the stock’s “Buy” rating. Sills cited a favorable risk-reward scenario, despite not expecting Q2 earnings to be a significant catalyst. Sills believes Workday is well-positioned to deliver above-market growth in the coming quarters, citing a balanced strategy, consistent pipeline builds, and ongoing subscription revenue momentum, which supports his bullish stance on the stock.

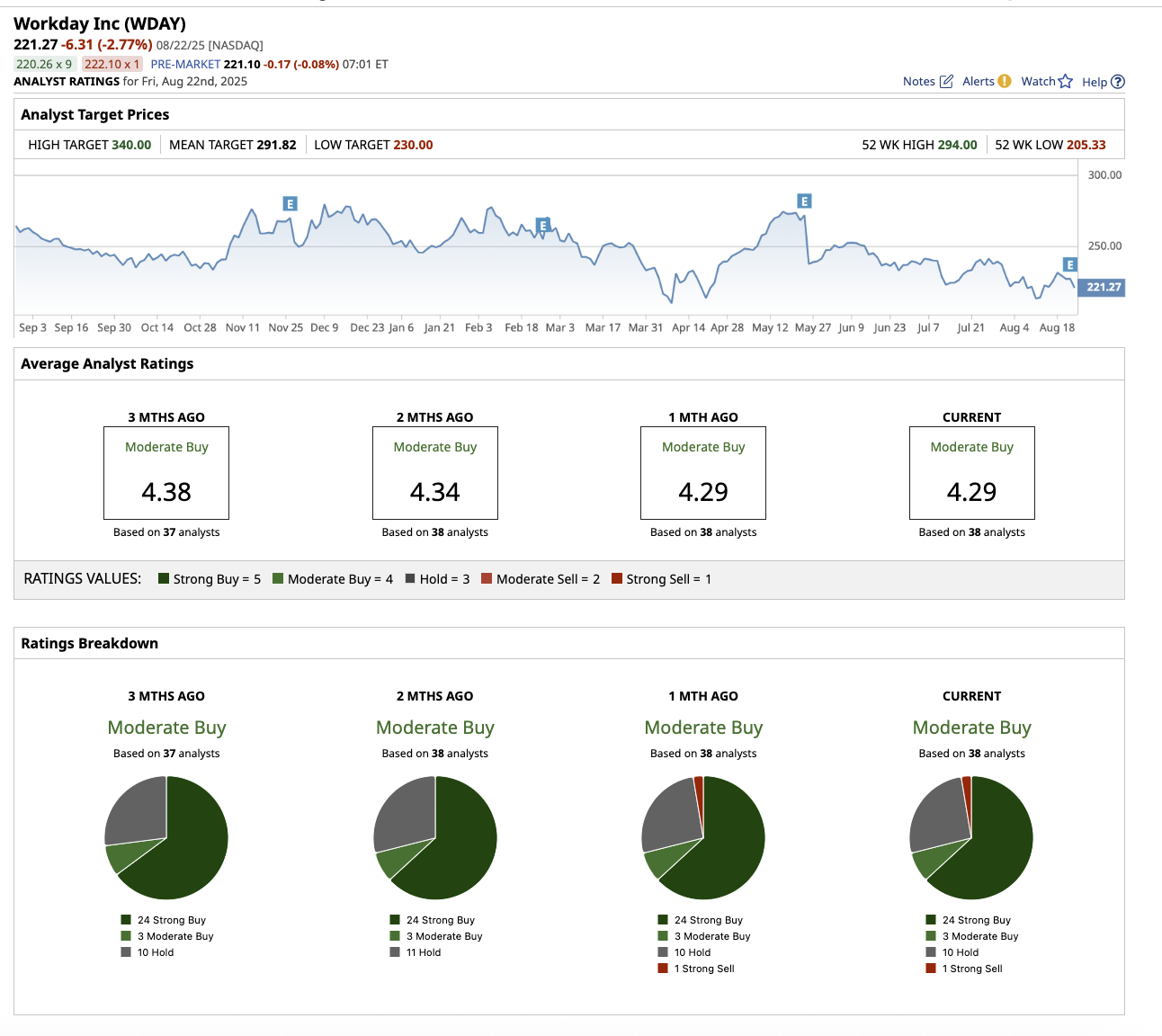

Overall, on Wall Street, analysts rate Workday stock as a “Moderate Buy.” Of the 38 analysts covering the stock, 24 rate it a “Strong Buy,” three say it is a “Moderate Buy,” 10 rate it a “Hold,” and one says it is a “Strong Sell.” The average target price of $291.82 implies the stock can rally as much as 30% over the next 12 months. The high price target of $340 suggests upside potential of 53.6% over the next 12 months.

On the date of publication, Sushree Mohanty did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.